The Rise of UPI : India's Digital Behaviour

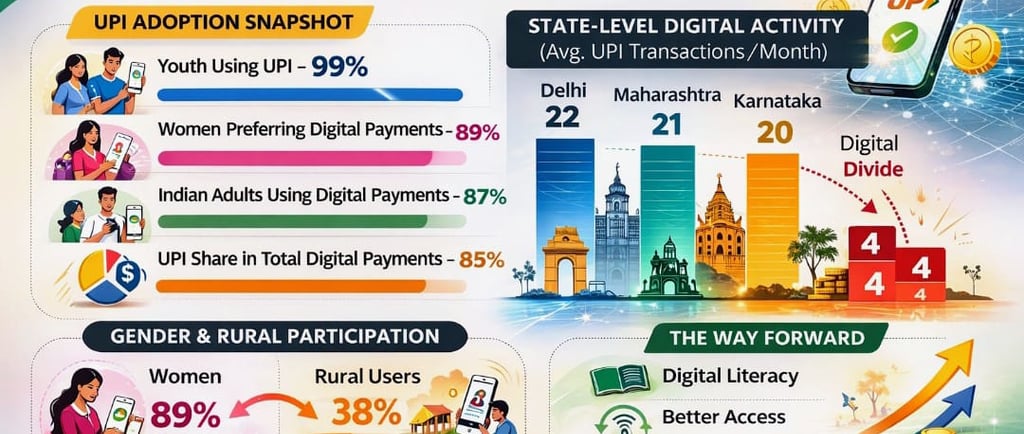

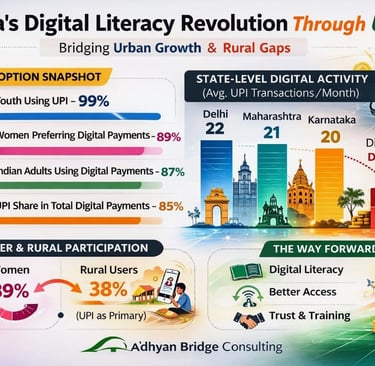

Over the past decade, India’s digital journey has evolved from a policy vision into an everyday reality. Driven by flagship programmes such as Digital India, the country has witnessed a steady expansion of broadband connectivity, rapid growth in digital payments, and deeper integration of online public services into daily life. With more than 800 million internet users and one of the youngest populations in the world, India today stands in a strong position to shape the future of the global digital economy. A central force behind this transformation has been the Unified Payments Interface (UPI), developed by the National Payments Corporation of India. UPI now contributes nearly 85% of the country’s total digital payment transactions. Additionally, close to 87% of Indian adults report using digital payment methods, placing India significantly ahead of many global benchmarks in terms of digital transaction penetration. These numbers reflect not just infrastructure growth, but a widespread behavioural shift toward digital-first financial practices. However, adoption patterns are not uniform across all demographics. Young Indians are leading this digital transition. Survey findings referenced by the Ministry of Statistics and Programme Implementation(MoSPI) indicate that nearly 99% of youth respondents use UPI for financial transactions. This suggests a high degree of comfort with app-based platforms, QR-code payments, and digital wallets among individuals under the age of 30. Gender participation has also shown positive momentum, especially in urban India. Industry insights reported by The Economic Times suggest that women are increasingly active participants in the digital economy. Approximately 89% of women prefer digital payment methods for online purchases, while nearly 80% of women entrepreneurs rely on digital tools for business-related payments. These trends point toward growing financial inclusion and rising digital confidence among women in metropolitan and Tier-2 cities. Despite this progress, disparities remain visible in rural and semi-urban regions. As per Economic Times Government around 38% of rural users consider UPI as their primary payment method. Yet, adoption among rural women continues to trail behind men, largely due to limited smartphone access, inconsistent connectivity, and gaps in digital literacy. The issue here extends beyond availability it relates to access, awareness, and sustained confidence. State-level variations further underline the digital divide. Metropolitan regions such as Delhi, Maharashtra, and Karnataka demonstrate high per-capita digital activity, with urban users averaging more than 20 UPI transactions per month. In contrast, eastern states like Bihar report significantly lower per-capita transaction volumes, often fewer than four transactions per person monthly in several districts. These differences reflect variations in digital infrastructure, merchant QR-code penetration, and user familiarity with digital tools. However, many rural districts continue to depend on assisted digital services or hybrid cash–digital systems, indicating a slower pace of independent adoption. The next stage must prioritise digital capability, user confidence, and inclusive participation across age groups, gender segments, and geographies. The sustainability of India’s digital future will depend on strengthening skills, trust, and meaningful usage across all sections of society. #DigitalIndia #UPI #DigitalPayments

Astha Anupam, Director, Adhyan Bridge Consulting

2/21/20261 min read

Bridging the gap between research, training, and advocacy to drive sustainable development and impactful change across sectors.

© 2026 Adhyan Bridge Consulting. All rights reserved.

Research | Training | Advocacy

Stay updated with our latest research and training programs.

Privacy Policy

Terms of Service